Myths vs. Facts in Modern Business Banking & Payments: Busting 6 Common Misconceptions

Digital

transformation is rapidly changing how businesses manage their banking and

payment processes. While technologies such as UPI, APIs, and AI-driven

analytics are becoming industry standards, a number of myths and misconceptions

still surround modern business banking. These misunderstandings often lead to

hesitation in adopting efficient, secure financial tools, causing businesses to

miss out on significant operational benefits.

This blog

aims to dispel six of the most common myths about business banking and

payments, helping you gain clarity and confidence in embracing digital

financial solutions that foster growth, security, and improved business

efficiency.

Table of Contents

1.

Myth

1: Digital Payments Are Less Secure Than Traditional Methods

2.

Myth

2: UPI and Instant Payment Systems Are Only for Consumers, Not Businesses

3.

Myth

3: Automation in Business Payments Means Losing Financial Control

4.

Myth

4: AI in Business Banking Is Too Complex for Small and Medium Enterprises

5.

Myth

5: Modern Payment Solutions Are Costly and Charge High Fees

6.

Myth

6: Payment Gateways and APIs Are Only Relevant for Large Enterprises

Detailed Myth Busting

Myth 1: Digital Payments Are Less Secure Than Traditional Methods

Fact: Digital payments today are secured

by advanced technologies such as end-to-end encryption, two-factor

authentication, and AI-powered fraud detection systems. Compared to paper

checks or cash payments, digital transactions significantly reduce risks related

to theft, fraud, and human error. For example, platforms with strong fraud

prevention protocols, like those discussed in the Fraud Prevention: Advanced Strategiesto Safeguard the Financial Ecosystem blog, offer enhanced security layers

that protect your business funds and data.

Myth 2: UPI and Instant Payment Systems Are Only for Consumers, Not Businesses

Fact: UPI (Unified Payments Interface) has

evolved from a consumer-focused payment system to a powerful platform

supporting business needs such as bulk payments, automated payroll, vendor

transactions, and instant collections. Businesses leveraging UPI APIs, as

outlined in the blogs on The UPIAPI Collection and Why UPICollection is Better Than a Payment Gateway, can enjoy faster settlement,

ease of use, and cost efficiencies compared to traditional payment systems.

Myth 3: Automation in Business Payments Means Losing Financial Control

Fact: Automation actually provides greater

control and transparency. Businesses benefit from reduced human error,

real-time transaction tracking, and extensive audit trails. With automated

systems, such as those discussed in What are Bulk Payments? – Benefits and How Does it Work?, companies can

streamline salary disbursements and vendor payments without sacrificing

oversight.

Myth 4: AI in Business Banking Is Too Complex for Small and Medium Enterprises

Fact: AI-powered dashboards are designed

to be user-friendly and insightful, helping SMEs forecast cash flow, detect

fraud, and optimize payment cycles without needing technical expertise. Tools

that incorporate AI for actionable insights are becoming standard in modern

payment platforms, as referred to in blogs on payment gateways and analytics.

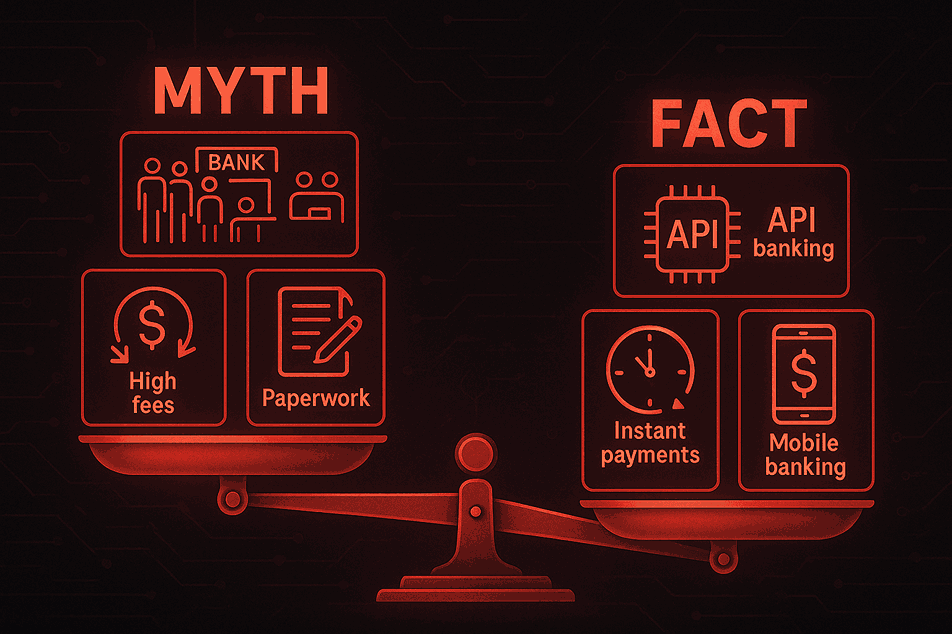

Myth 5: Modern Payment Solutions Are Costly and Charge High Fees

Fact: Digital payment solutions often

reduce overall costs by eliminating paper-based expenses, reducing processing

times, and minimizing errors that lead to financial losses. Many platforms

offer flexible, scalable pricing suited to business size and transaction

volume, enabling startups and SMEs to benefit without breaking the bank.

Myth 6: Payment Gateways and APIs Are Only Relevant for Large Enterprises

Fact: APIs and payment gateways empower

businesses of all sizes to integrate payments seamlessly with their existing

systems. Small businesses can automate collections and payouts, improve cash

flow management, and scale operations without heavy investments in IT

infrastructure. The blog on UltimateGuide to Payment Gateways in India highlights how accessible these

technologies are for all types of enterprises.

Conclusion

Modern

business banking and payment technologies present game-changing opportunities

for businesses of every size. By debunking these common myths, you can better

appreciate the security, convenience, cost-effectiveness, and scalability that

digital payment solutions offer. Embracing these tools not only streamlines

your financial operations but also positions your business competitively in a

fast-evolving market.

Frequently Asked Questions (FAQs)

Is UPI safe for business transactions?

Yes, UPI

uses secure authentication and encryption protocols trusted by millions of

merchants and businesses for instant and safe payments.

Can digital payment platforms handle payroll for thousands of employees?

Many

platforms support bulk payroll payments with automated disbursements,

simplifying salary payments for large workforces efficiently.

How quickly are failed digital payments resolved?

Most

platforms automate refunds and support quick dispute resolution, often

resolving issues within 24 to 72 hours.

Do businesses need technical expertise to use APIs?

No, many

platforms provide easy-to-use APIs with developer support and minimal setup,

accessible even to non-technical users.

What security measures protect my business from payment fraud?

AI-powered fraud detection, multi-factor authentication, and continuous transaction monitoring are standard features that secure your payments against fraud.